Verified Insights

Precision-driven research you can trust. We uphold rigorous data validation processes to ensure every report is reliable and based on credible sources.

+91 9425150513 (Asia) support@24lifesciences.com

MARKET INSIGHTS

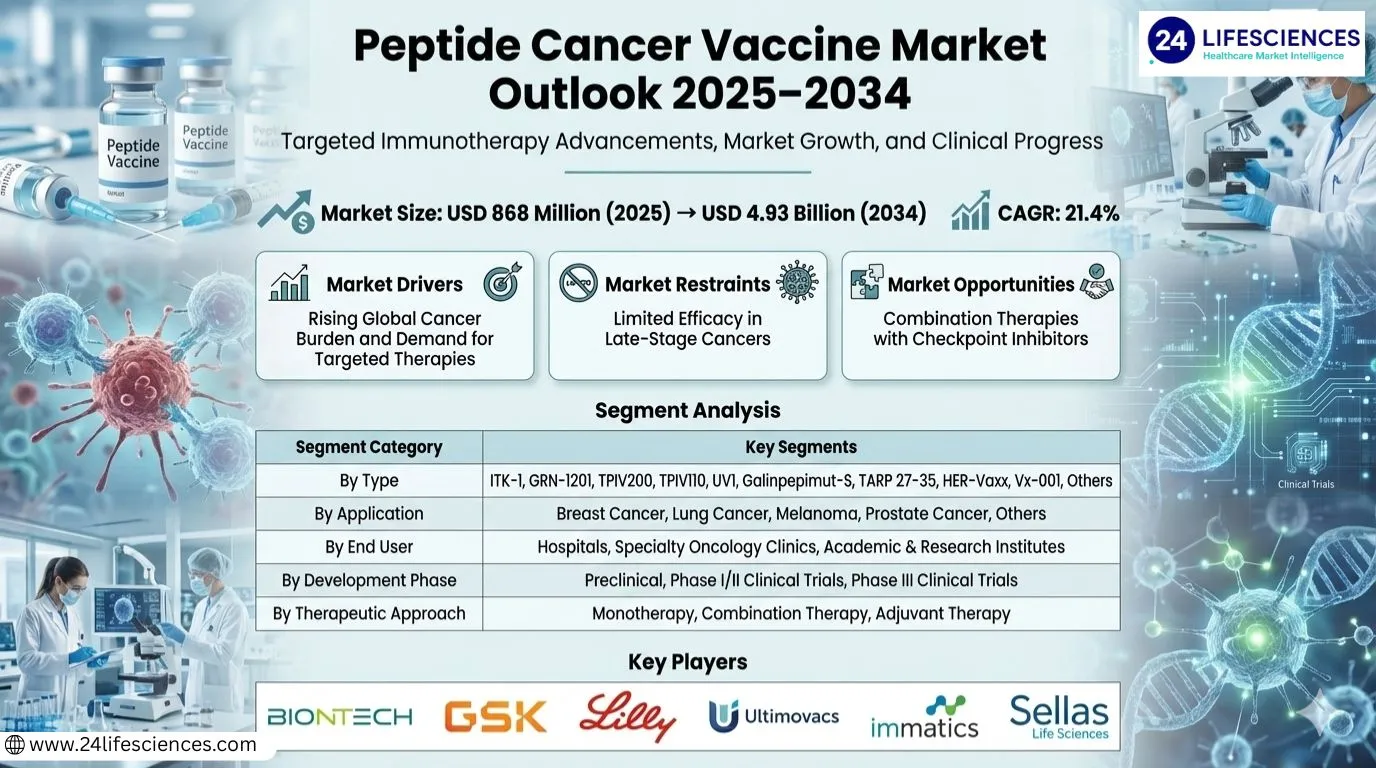

Peptide Cancer Vaccine market was valued at USD 868 million in 2025 and is projected to reach USD 4.93 billion by 2034, growing at a CAGR of 21.4% during the forecast period.

Peptide cancer vaccines represent a sophisticated form of immunotherapy designed to treat solid tumors. The fundamental mechanism of action involves administering specific peptides short chains of amino acids that are derived from or designed to mimic tumor-associated antigens. The primary objective is to stimulate a targeted T-cell immune response against cancer cells, either by generating a new response or by significantly boosting a pre-existing, yet insufficient, anti-tumor immunity within the patient.

The market's robust expansion is being driven by several powerful factors. Chief among them is the escalating global prevalence of cancer, coupled with a growing understanding of cancer immunology and a clear shift towards more targeted, personalized treatment modalities. Clinical research is particularly concentrated on melanoma, which accounts for approximately 40% of all peptide cancer vaccine research. North America dominates the market landscape, with the United States alone representing a substantial consumption share of nearly 53%, while Europe follows with a 31% share, reflecting strong clinical infrastructure and high R&D investment in these regions.

Rising Global Cancer Burden and Demand for Targeted Therapies

The increasing global incidence of cancer is a primary driver for the peptide cancer vaccine market. As traditional treatments like chemotherapy and radiation present significant side effects, there is a growing demand for targeted, less toxic immunotherapies. Peptide vaccines offer a personalized approach by activating the patient's immune system against specific tumor-associated antigens, making them an attractive option in oncology.

Technological Advancements in Vaccine Platforms

Significant progress in genomics, bioinformatics, and peptide synthesis technologies has accelerated the development of peptide cancer vaccines. Techniques for identifying neoantigens unique mutations in a patient's tumor allow for the creation of highly personalized vaccines. Furthermore, innovations in adjuvant systems and delivery mechanisms are enhancing the potency and efficacy of these vaccines.

Investments and Favorable Regulatory Policies

Substantial investments from both public and private sectors are fueling R&D activities. Regulatory agencies have shown increasing support for accelerated pathways for promising cancer immunotherapies. For instance, the FDA's Fast Track and Breakthrough Therapy designations are helping to bring novel peptide vaccines to market more quickly, responding to unmet medical needs.

MARKET CHALLENGES

High Development Costs and Complex Manufacturing

The personalized nature of many peptide cancer vaccines presents significant manufacturing challenges. Developing a unique vaccine for each patient requires sophisticated logistics, stringent quality control, and high production costs, which can limit scalability and commercial viability.

Other Challenges

Immune Evasion and Tumor Heterogeneity

Tumors can develop mechanisms to evade immune detection, and their heterogeneous nature means that a vaccine targeting specific antigens may not be effective against all cancer cells. This can lead to variable patient responses and limited therapeutic efficacy.

Stringent Regulatory Hurdles

Navigating the complex regulatory landscape for novel biologics is a major challenge. Demonstrating safety and efficacy in clinical trials, especially for personalized therapies, requires extensive data and can result in prolonged development timelines.

Limited Efficacy in Late-Stage Cancers

A significant restraint for the peptide cancer vaccine market is their often limited effectiveness in patients with advanced or metastatic disease. In these stages, the tumor microenvironment is highly immunosuppressive, which can hinder the vaccine's ability to initiate a robust and effective anti-tumor immune response.

Competition from Other Immunotherapies

The market faces strong competition from other established and emerging immunotherapies, such as immune checkpoint inhibitors, CAR-T cell therapies, and monoclonal antibodies. These alternatives often have broader indications and more proven clinical track records, which can overshadow the adoption of peptide vaccines.

Combination Therapies with Checkpoint Inhibitors

A major opportunity lies in combining peptide cancer vaccines with other immunotherapies, particularly immune checkpoint inhibitors. These combinations have the potential to overcome immunosuppressive barriers and create a synergistic effect, enhancing overall anti-tumor responses and improving patient outcomes in various cancer types.

Expansion into Neoadjuvant and Adjuvant Settings

There is significant potential for peptide vaccines in early-stage cancer treatment, used as neoadjuvant (before surgery) or adjuvant (after surgery) therapy. In these settings, the immune system is more competent, and the tumor burden is lower, which may lead to higher rates of prevention of recurrence and better long-term survival.

Growing Focus on Personalized Medicine

The global shift towards personalized medicine aligns perfectly with the development of neoantigen-based peptide vaccines. Advances in next-generation sequencing and computational biology are making it increasingly feasible to develop truly personalized vaccines, opening up substantial market opportunities in tailored cancer care.

Segment Analysis:| Segment Category | Sub-Segments | Key Insights |

| By Type |

| UV1 is demonstrating significant promise as a leading candidate in clinical development, attracting considerable attention from researchers and investors for its innovative mechanism. This personalized vaccine platform is designed to elicit a robust T-cell response against a universal cancer antigen, showing potential for treating various solid tumors. The high level of clinical activity surrounding UV1 underscores a strategic trend towards developing adaptable therapeutic platforms that can be tailored to individual patient needs, which is a key area of focus for advancing personalized cancer immunotherapy and improving long-term patient outcomes. |

| By Application |

| Melanoma serves as the cornerstone application for peptide cancer vaccine research, representing the most extensively studied and validated indication. The well-characterized tumor antigens and the immunogenic nature of melanoma make it an ideal candidate for this immunotherapeutic approach. The substantial body of clinical evidence and ongoing trials in melanoma provide crucial proof-of-concept, driving innovation and establishing treatment paradigms that are increasingly being explored for application in other cancer types with high unmet medical needs, thereby expanding the therapeutic horizon. |

| By End User |

| Academic & Research Institutes are the primary drivers of innovation and early-stage clinical development in the peptide cancer vaccine market. These institutions are at the forefront of basic science discovery, target identification, and initial clinical trial execution, generating the foundational data required for therapeutic advancement. Their critical role in pushing the boundaries of knowledge and translating laboratory findings into clinical protocols makes them indispensable for the long-term growth and validation of the entire market, fostering a pipeline of next-generation treatments. |

| By Development Phase |

| Phase I/II Clinical Trials represent the most active and dynamic segment of the market, where the majority of investigational peptide vaccines are currently being evaluated. This phase is critical for demonstrating initial safety, determining optimal dosing, and providing early signals of clinical efficacy. The high concentration of assets in this stage reflects the intense research activity and investment aimed at proving therapeutic concepts, with successful outcomes here being a key gateway to larger, more definitive Phase III studies and eventual regulatory approval and commercial viability. |

| By Therapeutic Approach |

| Combination Therapy is emerging as the predominant and most promising strategic approach, where peptide vaccines are used alongside other immunotherapies like checkpoint inhibitors or conventional treatments. This strategy aims to overcome tumor-induced immunosuppression and create a synergistic anti-cancer effect, enhancing the potency and durability of the immune response. The focus on combinations represents a major evolution in treatment strategy, moving beyond standalone vaccines to integrated regimens that are expected to define the future standard of care and unlock greater clinical benefits for patients. |

A Fragmented Market Poised for Strategic Consolidation and Growth

The Peptide Cancer Vaccine market is characterized by a dynamic and fragmented competitive landscape, dominated by a mix of specialized biotechnology firms and pharmaceutical companies focusing on innovative immuno-oncology platforms. Leading players such as Immatics and Ultimovacs have established strong positions through their advanced T-cell receptor and universal cancer vaccine technologies, respectively. Many of these key players are distinguished by their robust and diverse clinical pipelines targeting a range of solid tumors, particularly melanoma, which represents the largest application segment. The competitive intensity is high, with companies vying for first-mover advantage in late-stage clinical trials and strategic partnerships with larger pharmaceutical entities to accelerate development and commercialization. Market leadership is primarily driven by technological innovation, intellectual property portfolios, and successful clinical trial outcomes that validate the efficacy of their peptide vaccine candidates.

Beyond the established front-runners, a significant number of companies operate in specific niches or with platforms tailored to particular cancer antigens. Firms like Sellas Life Sciences, with its Wilms' Tumor 1 (WT1) targeting vaccine, and ISA Pharmaceuticals, specializing in Synthetic Long Peptide (SLP) technology, exemplify this focused approach. Other notable participants, including VAXON Biotech and BrightPath Biotherapeutics, contribute to the market's diversity with their unique adjuvant systems and delivery platforms designed to enhance immune responses. While North America, led by the USA, is the largest market, European companies also hold a substantial share, contributing to a globally competitive environment. The market is also witnessing increased activity from companies in Asia, adding another layer of competition. This landscape is anticipated to evolve significantly as clinical data matures, potentially leading to consolidation through mergers and acquisitions.

List of Key Peptide Cancer Vaccine Companies ProfiledBoston Biomedical

BrightPath Biotherapeutics

TapImmune (acquired by Marker Therapeutics)

Imugene

VAXON Biotech

Generex Biotechnology

ISA Pharmaceuticals

OncoTherapy Science

Eli Lilly and Company (through acquisition)

GSK

CureVac

BioNTech SE

Peptide Cancer Vaccine market is on a trajectory of significant expansion, with a valuation of $715 million in 2024 projected to surge to over $2.7 billion by 2031. This represents a robust compound annual growth rate (CAGR) of 21.4%. This growth is fundamentally driven by the increasing adoption of immunotherapy as a primary modality for treating solid tumors. Peptide-based vaccines function by generating a targeted T-cell immune response against cancerous cells or by amplifying the body's pre-existing antitumor immunity. The high specificity of this approach, which aims to minimize damage to healthy cells, is a key factor propelling research, investment, and clinical adoption.

Other TrendsDominance of Melanoma and Key Regional Markets

Application-specific trends reveal that melanoma is the most prominent area of research and development for peptide cancer vaccines, accounting for approximately 40% of the market focus. This is followed by significant efforts targeting breast cancer, lung cancer, and prostate cancer. Geographically, the market is highly concentrated, with the United States being the largest consumption region, holding a dominant market share of nearly 53%. Europe follows as the second-largest market, accounting for 31% of global consumption, underscoring the advanced healthcare infrastructure and significant R&D investments in these regions.

Competitive Landscape and Pipeline InnovationThe competitive environment is characterized by specialized biotechnology firms driving innovation. Key manufacturers include Boston Biomedical, Ultimovacs, BrightPath Biotherapeutics, TapImmune, Immatics, Sellas, and Imugene, among others. The market's dynamism is evident in its diverse and evolving pipeline, with numerous candidates in various stages of clinical development. Prominent pipeline products such as GRN-1201, TPIV200, UV1, and Galinpepimut-S represent the next wave of potential therapeutic options. The ongoing development and clinical trial outcomes for these candidates are critical trends that will shape future market leadership and therapeutic availability across different cancer indications.

Regional Analysis: Peptide Cancer Vaccine MarketEurope

Europe represents a significant and mature market for peptide cancer vaccines, characterized by strong governmental support for cancer research and a well-organized healthcare system. Countries like Germany, the UK, and France are at the forefront, with numerous research initiatives funded by national and EU programs. The European Medicines Agency provides a centralized approval pathway, though market access can vary between member states. There is growing emphasis on personalized medicine, aligning well with the targeted nature of peptide vaccines. However, cost-containment pressures and stringent pricing regulations pose challenges to market growth compared to North America, necessitating clear demonstration of clinical value and cost-effectiveness for new vaccine approvals.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for peptide cancer vaccines, driven by increasing cancer prevalence, rising healthcare expenditure, and improving medical infrastructure. Japan and China are key contributors, with strong government initiatives to boost domestic biopharmaceutical capabilities and a growing number of clinical trials. The large patient population provides a substantial base for vaccine development and adoption. While regulatory pathways are evolving and becoming more streamlined, heterogeneity in healthcare systems and reimbursement policies across countries creates a varied market landscape. Local manufacturing growth and increasing international collaborations are expected to significantly propel the market forward in the coming years.

South America

South America's peptide cancer vaccine market is in a developing phase, with Brazil and Argentina showing the most promise. Market growth is primarily driven by increasing awareness of cancer immunotherapy and gradual improvements in healthcare infrastructure. However, economic volatility and budget constraints in public health systems often limit patient access to advanced and costly treatments. Clinical research activity is growing, supported by collaborations with international organizations, but the region still relies heavily on imported therapies. The market potential is significant due to the unmet medical need, but realizing this potential depends on economic stability and strengthened local regulatory and healthcare frameworks.

Middle East & Africa

The Middle East & Africa region presents a nascent but emerging market for peptide cancer vaccines. The Gulf Cooperation Council countries, with their higher healthcare spending, are leading the adoption of advanced oncology treatments. Initiatives to improve cancer care centers and attract medical tourism are creating opportunities. However, the broader region faces significant challenges, including limited healthcare infrastructure, lower awareness of novel immunotherapies, and constrained funding for expensive treatments. Market growth is uneven, concentrated in wealthier nations, while access remains a major hurdle across most of Africa. International aid and partnerships are crucial for building capacity and introducing these innovative therapies to the region.

This market research report offers a holistic overview of global and regional markets for the forecast period 20252031. It presents accurate and actionable insights based on a blend of primary and secondary research.

Market Overview

Global and regional market size (historical & forecast)

Growth trends and value/volume projections

Segmentation Analysis

By product pipeline (ITK-1, GRN-1201, TPIV200, etc.)

By application (Breast Cancer, Lung Cancer, Melanoma, etc.)

By end-user segment

Regional Insights

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa

Country-level data for key markets (USA, Germany, China, etc.)

Competitive Landscape

Company profiles and market share analysis

Key strategies: M&A, partnerships, R&D

Product portfolio and clinical trial progress

Technology & Innovation

Emerging immunotherapy technologies

Personalized medicine approaches

Advancements in peptide vaccine design

Market Dynamics

Key drivers supporting market growth

Regulatory challenges and clinical trial risks

Supply chain considerations for biologics

Opportunities & Recommendations

High-growth cancer segments

Investment hotspots in immunotherapy

Strategic suggestions for stakeholders

Stakeholder Insights

This report is designed to support strategic decision-making for a wide range of stakeholders, including:

Pharmaceutical and biotech companies

Medical research institutions

Healthcare providers and oncology centers

Contract research organizations

Investors and venture capitalists

-> Peptide Cancer Vaccine market was valued at USD 868 million in 2025 and is projected to reach USD 4.93 billion by 2034, growing at a CAGR of 21.4% during the forecast period.

Which key companies operate in Global Peptide Cancer Vaccine Market?

-> Key players include Boston Biomedical, Ultimovacs, BrightPath Biotherapeutics, TapImmune, and Immatics, among others.

-> Key growth drivers include rising cancer prevalence, advances in immunotherapy, and increasing R&D investments.

-> North America holds the largest market share (53%), followed by Europe (31%).

-> Melanoma dominates research (40% share), followed by breast cancer, lung cancer and prostate cancer.

“The data provided by 24LifeScience was clear, well-organized, and useful for internal strategy planning. It helped us understand the competitive landscape more effectively.”

“We used one of their market overview reports for early-stage feasibility work. It gave us a helpful snapshot of current trends and key players in our therapeutic area.”

“I appreciated the team’s responsiveness and willingness to adjust the scope based on our feedback. The final report was aligned with our expectations and timelines.”

“Their custom report on clinical trial trends was a helpful reference as we explored new indications."

“As someone working on early product planning, I found their therapeutic area briefs quite useful. The information was presented in a way that made it easy to extract key takeaways.”

“We didn’t need anything overly complex—just solid, dependable data. 24LifeScience delivered exactly that, without unnecessary fluff.”

“Their reports gave us a good foundation to start our own market assessment. While we supplemented it with other data, this was a great starting point.”

“I’ve used a few of their reports for academic and grant writing purposes. They’re generally well-cited and reliable for understanding market scope.”

At 24LifeScience, we combine domain expertise with dependable research delivery. What truly differentiates us isn't just what we do — it's how we do it. Our clients trust us because we offer consistency, security, value, and most importantly, insight that drives action.

Precision-driven research you can trust. We uphold rigorous data validation processes to ensure every report is reliable and based on credible sources.

We uphold rigorous data validation processes to ensure every report is reliable, up-to-date, and based on credible sources.

24LifeScience powers research for top firms in 20+ nations.Chosen by leading life sciences companies worldwide.

We offer competitive pricing models that align with your project scope — no hidden charges, no lock-in. Tailored pricing for every scale and need.

8–10+ years of life sciences expertise turned into strategic insights.We don’t just summarize data we contextualize it.

Whether it's a ready-made report or a custom project, we deliver within the promised timeline With real-time updates